TCFD Issues New Guidance as Its Climate Reporting Framework Continues to Gain Traction

As detailed in a recent Financial Stability Oversight Council report, climate change is widely seen as posing systemic risks to financial and economic stability, leading investors and regulators to push for more comprehensive voluntary and mandatory climate risk disclosures.

The voluntary disclosure framework laid out in the 2017 Recommendations of the industry-led Task Force on Climate-related Financial Disclosures (“TCFD”) stands out among environmental, social and governance (“ESG”) frameworks for the extent to which financial regulators and market participants have coalesced around it. According to the TCFD’s recently released 2021 Status Report, the TCFD’s Recommendations now have over 2,600 supporters worldwide — an increase of over 70% since the 2020 Status Report.

The TCFD’s Recommendations have been endorsed by twelve governments (including the EU, UK and Hong Kong) alongside dozens of central banks, supervisors and regulators. Moreover, as set out below, several jurisdictions are already transitioning from encouraging the voluntary adoption of the Recommendations to mandating TCFD-aligned disclosure.

This level of consensus makes the TCFD’s two recent updates to the Annex on Implementing the Recommendations and Guidance on Metrics, Targets and Transition Plans noteworthy.

Given the TCFD’s market influence and the emergence of mandatory TCFD-aligned disclosure in key jurisdictions, companies and financial institutions may benefit from working with counsel to carefully review this new TCFD guidance and consider the implications for their existing climate risk assessment, reporting and governance structures.

Overview of TCFD Updates

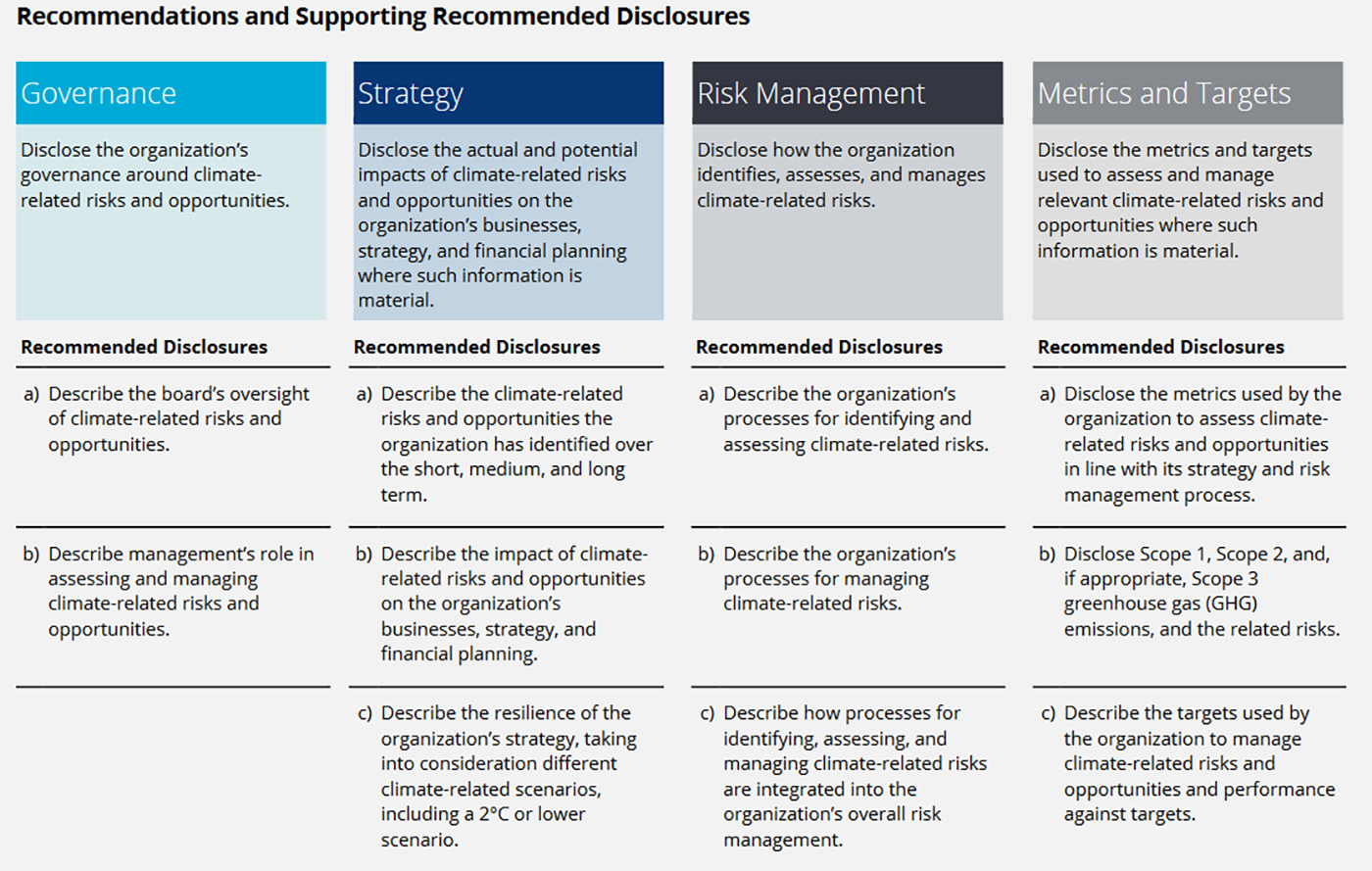

The TCFD framework identifies eleven topics organized under four broad categories — “Governance,” “Strategy,” “Risk Management” and “Metrics and Targets” — that firms can use to assess and report on climate risks and opportunities. This is detailed below.

TCFD Framework1

Since the TCFD issued its Recommendations in 2017, market and regulatory attention has increasingly focused on disclosure of climate-related metrics and targets (see Implications below). However, companies making TCFD disclosures have reported that the “Metrics and Targets” recommended disclosures are “somewhat difficult” or “very difficult” to implement.

To address recent market developments and feedback following public consultations held between October 2020 and July 2021, in October 2021 the TCFD released additional Guidance on Metrics, Targets and Transition Plans. To reflect this guidance, the TCFD also issued an updated Annex on Implementing the Recommendations (“Annex”), which supersedes the 2017 version. The updated Annex includes modified guidance for the “Strategy” and “Metrics and Targets” disclosure categories, in line with the Guidance on Metrics, Targets and Transition Plans.

Together, these documents encourage more specific disclosures in alignment with the TCFD’s framework, which may form the basis for both voluntary investor reporting requests and mandatory regulatory requirements going forward.

In the words of the TCFD Secretariat: "As countries and companies around the world set net zero targets, the TCFD framework is increasingly becoming the foundation for standards and requirements needed to chart the transition to the low-carbon economy.”

Annex on Implementing the Recommendations

The TCFD’s revised Annex contains guidance for companies on how they can implement the Recommendations (which remain unchanged), updated to reflect the new Guidance on Metrics, Targets and Transition Plans.

The most notable change to the Annex centers on emissions disclosures, pursuant to Recommended Disclosure b) under “Metrics and Targets.” While disclosures in the “Strategy” and “Metrics and Targets” categories generally remain subject to a materiality assessment, the TCFD now recommends that all organizations disclose their Scope 1 and 2 emissions independent of an assessment of materiality.2 Although the more challenging disclosure of Scope 3 emissions remains subject to materiality, the TCFD encourages all organizations to disclose these emissions — including, for the financial sector, emissions associated with lending, underwriting, asset management and investing activities. For greenhouse gas (“GHG”) emissions accounting, the TCFD endorses the use of the Global GHG Accounting and Reporting Standard for the Financial Industry, developed by the Partnership for Carbon Accounting Financials (“PCAF”)3.

Additionally, the Annex recommends that financial institutions disclose the extent to which their lending, underwriting, asset management and investing activities “are aligned with a well below 2°C scenario” (i.e. portfolio alignment), pursuant to Recommended Disclosure a) under “Metrics and Targets.”

Other noteworthy changes in the Annex include:

- with respect to Recommended Disclosure c) under “Metrics and Targets”, a call for disclosure of interim targets4 by organizations disclosing medium- or long-term targets; and

- with respect to Recommended Disclosures b) and c) under “Strategy,” more explicit calls for disclosure of potential financial impacts from climate change and plans for transitioning to a low-carbon economy.

Guidance on Metrics, Targets and Transition Plans

The TCFD’s Guidance on Metrics, Targets and Transition Plans builds on the TCFD’s existing Recommendations and guidance. The new guidance provides additional context on selecting climate-related metrics and targets to report, as well as instructions on the disclosure of climate-related financial impacts and transition plans (as called for by the Annex).

Climate-Related Metrics

The TCFD defines effective climate-related metrics as those which are 1) decision-useful, 2) clear and understandable, 3) reliable, verifiable and objective, and 4) consistent over time. It has identified seven categories of metrics that all organizations should disclose, in order to enable comparisons within and across industries. These are:

- GHG Emissions, including Scope 1, Scope 2 and Scope 3 emissions, as well as emissions intensity metrics (e.g., emissions per unit of energy produced);

- Transition Risks, such as percentage of revenue from coal mining or credit exposure to carbon-intensive assets;

- Physical Risks, such as revenue associated with water withdrawn from areas with high water stress or proportion of assets in areas subject to extreme climate events;

- Climate-Related Opportunities, such as number of zero-emissions vehicles sold or proportion of homes delivered certified to a third-party green building standard;

- Capital Deployment, such as investment in climate adaptation measures or percentage of annual revenue invested in development of low-carbon products or services;

- Internal Carbon Price, which could be the same firm-wide or vary by geography; and

- Remuneration, such as the weighting of performance against operational emissions for remuneration scorecards or proportion of employees’ annual discretionary bonuses linked to investments in climate-related products.

Climate-Related Targets

The TCFD has added greater specificity on the disclosure of climate-related target setting, particularly on GHG emissions. Climate-related targets are specific goals for selected milestones that organizations aim to meet to address their climate-related risks and opportunities. The TCFD recommends, among other things, that targets be aligned with an organization’s strategy and risk management goals, quantified and measurable where possible, defined within clear time horizons (with medium- and long-term goals supported by interim goals), and updated at least every five years. Additionally, the TCFD calls for targets to be supported by contextual, narrative information on items such as organizational boundaries, methodologies and underlying data and assumptions, including context on the use of offsets to meet GHG reduction goals. The TCFD also counsels against assuming climate-related targets contain confidential business information, and encourages organizations to “provide relevant information in broader terms” when a target is determined to be confidential.

Transition Plans

The TCFD has also included additional guidance for organizations developing and disclosing transition plans to implement their climate-related targets, plus guidance for disclosing the actual or potential financial impacts of climate-related risks and opportunities. While the TCFD notes that transition plans will have industry-specific nuances, it asserts that effective plans are, among other things: aligned with an organization’s broader business strategy, subject to effective governance, actionable and specific with achievable milestones, contextualized to an organization’s capabilities and restraints, and updated at least every five years. The TCFD also provides examples of disclosures of specific financial impacts of climate change — such as increases in cost due to carbon prices, business interruption, contingency or repairs — and notes that such impact disclosures may depend on the transition plans an organization has in place.

Implications

The TCFD framework features prominently in several emerging, climate-related financial regulatory requirements. For example:

- The United Kingdom in November 2020 released a Roadmap towards mandatory TCFD-aligned disclosures across UK economic actors by 2025. The Financial Conduct Authority (“FCA”) issued a rule requiring commercial companies with a UK premium listing to disclose, on a comply-or-explain basis, against the four pillars of the TCFD for accounting periods beginning in 2021. As part of the Roadmap, the FCA has also issued proposed rules (with finalized rules expected this year) that would extend this requirement to other listed companies, asset managers, life insurers and FCA-regulated pension providers consistent with the Roadmap’s 2025 timeframe. In addition, the FCA published a discussion paper on November 3, 2021 seeking market views on a potential three-tiered system incorporating labels and disclosures, which will seek to build on the proposed TCFD-aligned disclosure requirements. Separately, on October 28, 2021, the UK Department for Business, Energy & Industrial Strategy announced plans to require TCFD-aligned disclosures by publicly quoted companies, large private companies and LLPs beginning in April 2022.

- The European Union in June 2019 published a supplement on reporting climate-related information as part of its guidance on reporting under the Non-Financial Reporting Directive (“NFRD”), which integrates the core pillars of the TCFD’s recommendations. The successor regime to the NFRD, the Corporate Sustainability Reporting Directive (“CSRD”), would have a broader remit, applying to nearly 50,000 large companies with organizational presence in the EU. The first report by EFRAG, the organization tasked with developing the new CSRD disclosure standard, notes that the TCFD-compatible disclosures will form part of an “advanced” standard.

- The Hong Kong Stock Exchange amended its listing rules, effective July 2020, to require mandatory TCFD-aligned reporting for all listed companies. In December 2020, the Hong Kong Green and Sustainable Finance Cross-Agency Steering Group announced that TCFD-aligned disclosures will be mandatory across relevant financial sectors by 2025.

- Japan’s Tokyo Stock Exchange published a revision to its Corporate Governance Code in June 2021, introducing TCFD-aligned climate disclosure requirements, and Japan’s Financial Services Agency will require companies listed on the Tokyo Stock Exchange to comply with TCFD-aligned disclosure requirements beginning in April 2022 (for large companies) or 2023 (for other companies).

Additionally, as discussed in our recent Alert, U.S. Securities and Exchange Commission (“SEC”) Chair Gary Gensler has reportedly asked staff to look to the TCFD in formulating a proposed climate reporting rule for U.S. companies.

As outlined above, the TCFD’s new Annex could influence both existing and emerging regulatory reporting requirements. For example, Chair Gensler has said that he has asked SEC staff to make recommendations about whether, and under what circumstances, companies should be required to disclose their Scope 3 emissions. Given the TCFD’s preeminence, the TCFD’s new guidance encouraging Scope 3 emissions disclosure, subject to a materiality assessment, could influence SEC staff in making this decision. Additionally, the TCFD’s support for and guidance around transition plans could influence the UK’s development of its Sustainability Disclosure Requirements, which the aforementioned Roadmap indicates will be part of the country’s new regulatory regime. And the TCFD framework is relevant to the International Financial Reporting Standard (“IFRS”) Foundation’s establishment of a new standard-setting board, the International Sustainability Standards Board (“ISSB”), to develop sustainability disclosure rules alongside the IFRS accounting standards.

In addition to potentially influencing regulations, the TCFD’s new guidance could be leveraged by investors who are pushing companies to enhance their climate disclosures. The TCFD is supported by several influential investor groups, such as the Principles for Responsible Investment (which has incorporated certain elements of the TCFD framework into its reporting template), Climate Action 100+ (whose Benchmark assessment has an indicator on the implementation of TCFD-aligned disclosure), and the Investor Agenda (whose $52 trillion group of 733 investors recently called on governments to commit to implementing mandatory TCFD-aligned disclosure requirements at COP26). These, and other groups, may draw on the new Annex in pushing for more widespread and detailed climate-related disclosures.

These evolving expectations could pose challenges for some companies, but they also create opportunities for proactive firms to demonstrate climate leadership. The TCFD’s 2021 Status Report reviewed disclosures by 1,651 public companies from 69 countries and jurisdictions, finding that, while disclosure of information in line with TCFD’s recommendations is increasing, only around half of companies disclosed against at least three of the TCFD’s eleven recommended disclosures and only 13% disclosed the resilience of their strategies under different climate scenarios (Recommendation Disclosure c) under “Strategy”).

Given the speed with which regulatory requirements and investor expectations are shifting, companies and financial institutions can benefit from working with counsel to enhance their climate governance and assess their existing risks, opportunities, strategies and disclosures against the TCFD framework.

1. TCFD Recommendations report Figure 4, available at https://assets.bbhub.io/company/sites/60/2021/10/FINAL-2017-TCFD-Report.pdf.↩

2. The revised Annex indicates that this change was the subject of disagreement among TCFD members, with some preferring to keep Scope 1 and 2 emissions disclosures subject to materiality.↩

3. The TCFD notes that the PCAF accounting standard currently does not provide guidance on calculating GHG emissions for certain financial products, including: private equity investment funds, green bonds, sovereign bonds, loans for securitization, exchange traded funds, derivatives and initial public offering underwriting. The PCAF notes “guidance on such financial products will be considered and published in later editions of the Standard.” The TCFD “encourages asset owners to disclose GHG emissions for additional financial products, where data are available or can be reasonably estimated, as methodologies are published.”↩

4. Some companies are beginning to develop transition plans with interim targets as part of a shift towards breaking down longer-term emission reduction trajectories into dedicated goals for different phases. ↩