Restructuring Update: UK Budget and Increase of “Prescribed Part”

Today’s UK Budget saw two changes particularly relevant for the restructuring and insolvency market: the delay of the planned return of HMRC as a preferential creditor and the temporary abolition of business rates for the retail, leisure and hospitality sectors below a certain (low) threshold. Separately, the government has published legislation increasing the amount of the “prescribed part” — a ring-fenced sum made available to unsecured creditors from floating charge realisations.

At a glance

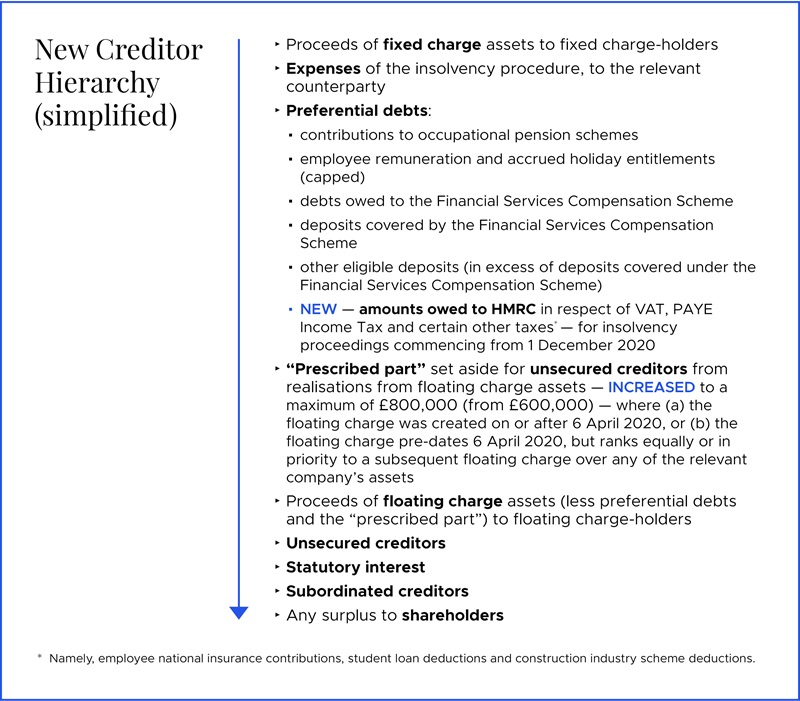

- HMRC’s return as preferential creditor: The return of HMRC as a secondary preferential creditor in insolvency proceedings (in respect of certain taxes) will be delayed until 1 December 2020. Once implemented, this reform is expected to increase HMRC’s influence in distressed situations and decrease creditors’ appetite to lend based on floating charge security (or on an unsecured basis).

- Business rates: Abolished for firms in the retail, leisure and hospitality sectors for properties with a rateable value below £51,000, for one year.

- Prescribed part: The ring-fenced sum made available to unsecured creditors from floating charge realisations will increase from £600,000 to £800,000 where the relevant floating charge was created on or after 6 April 2020.1

HMRC’s return as preferential creditor

The Budget announced that the government will delay plans to install HMRC as secondary preferential creditor in an insolvency for debts relating to certain taxes paid by employees and customers. The measures will now take effect in respect of formal insolvencies commencing from 1 December 2020, rather than 6 April 2020 as previously announced.

Draft legislation for the measure (which was first trailed in the autumn 2018 budget) was originally published in July 2019. The measure faced co-ordinated pressure from business groups, insolvency experts, the financial and legal sectors2 as to the potential damage this measure could cause to UK business and the UK’s corporate rescue culture. The delay perhaps offers some hope that the measure may in due course be dropped altogether.

Key takeaways

- In insolvency proceedings commencing from 1 December 2020, HMRC will rank ahead of both floating charge holders and unsecured creditors in an insolvency in respect of:

- VAT;

- PAYE Income Tax;

- employee National Insurance contributions; and

- Construction Industry Scheme deductions.

HMRC will remain an unsecured creditor in respect of all other taxes, including, e.g., corporation tax.

- This is a partial reversal of the abolition of HMRC’s preferential status in 2003. The move is controversial, as it effectively increases HMRC’s share of insolvent estates, which will reduce returns to unsecured creditors (which, on average, are already only 4p/£). The impact of the reform will be somewhat mitigated by the increase in the prescribed part set aside for unsecured creditors, from £600,000 to £800,000. However, these reforms represent a "double whammy" hit to floating charge holders.

Expected impact (once effective)

- This change is expected to result in higher financing costs for UK companies, as prospective creditors seek to reduce their exposure on any insolvency via a move toward more fixed-charge and asset-based lending.3

- The reform looks set to give HMRC additional influence in insolvency processes. Existing restrictions on compromising preferential debts within a company voluntary arrangement without the consent of the preferential creditors may hand HMRC a de facto veto over certain CVAs, making it more difficult for struggling companies to shed sufficient of their liabilities to enable a return to financial health.

Business rates

The government had already announced that, for one year from 1 April 2020, the business rates retail discount for properties with a rateable value below £51,000 in England would increase from 1/3 to 50%. To support small businesses, in response to COVID-19, the discount will be increased to 100% and expanded to include hospitality and leisure businesses for 2021. The Budget also announced the launch of a fundamental review of business rates, to report in autumn 2020.

The government’s action on business rates, which raise £31 billion annually, comes following substantial pressure from the retail sector. The high street is being increasingly squeezed, with long-term factors including online competition being supplemented by shorter-term factors, including sustained bad weather in the early months of 2020 and, more recently, the spectre of COVID-19 significantly impacting footfall.

The reform should afford relevant businesses some welcome breathing space — although it is likely to have little effect on larger retailers, whose properties are likely to have a rateable value above £51,000 — but who are major employers and (presumably) similarly affected by the impact of COVID-19.

1. The reform also captures a floating charge created before 6 April 2020 if a later floating charge (over any of the company’s assets) ranks equally or in priority. See the full text of The Insolvency Act 1986 (Prescribed Part) (Amendment) Order 2020. ↩

2. Including a joint statement published ahead of the budget. ↩

3. See, for example, the letter from R3 and other stakeholders. ↩